Conforming MortgagesNovember 30, 2010

2011 Conforming Mortgage Loan Limits By County, Including “Normal” and “High-Cost” Areas

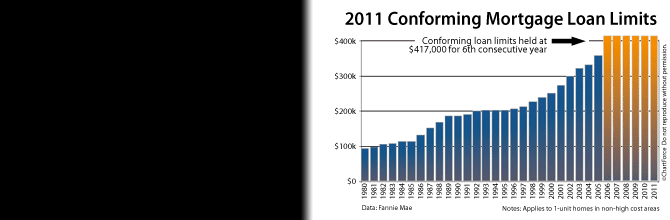

In 2011 -- for the 6th consecutive year -- the single-family conforming mortgage loan limit will be $417,000. The "high-cost" area program is extended, too.