Federal ReserveJune 19, 2019Mortgage rates fall as the Fed hints at future rate cutsMortgage rates are in a tailspin as the Fed holds rates steady in June and hints at a significant cut this July.

Federal ReserveMarch 20, 2019March 2019 Fed meeting: Mortgage rates fall as Fed scraps plans for future rate hikesMortgage rates plummet after a surprise move by the Fed: a forecast of no more rate hikes in 2019.

Federal ReserveJanuary 30, 2019January 2019 Fed meeting: Committee says inflation not yet a concern, rates unchangedThis month's Fed meeting provided few surprises. No interest rate increase, but it's still on the table for December.

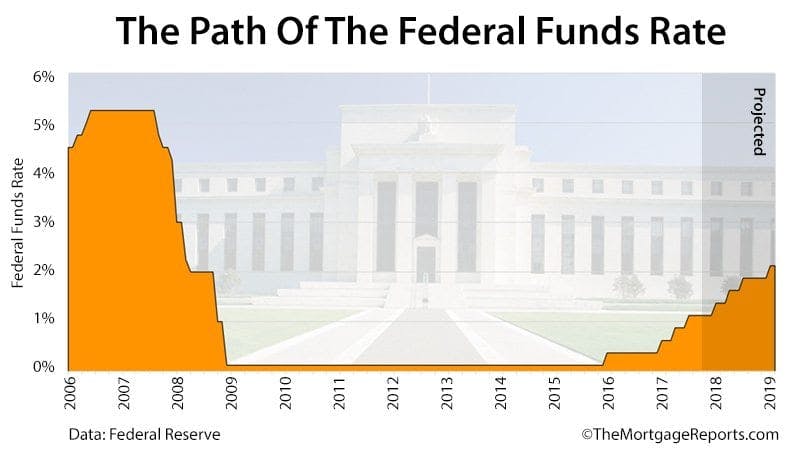

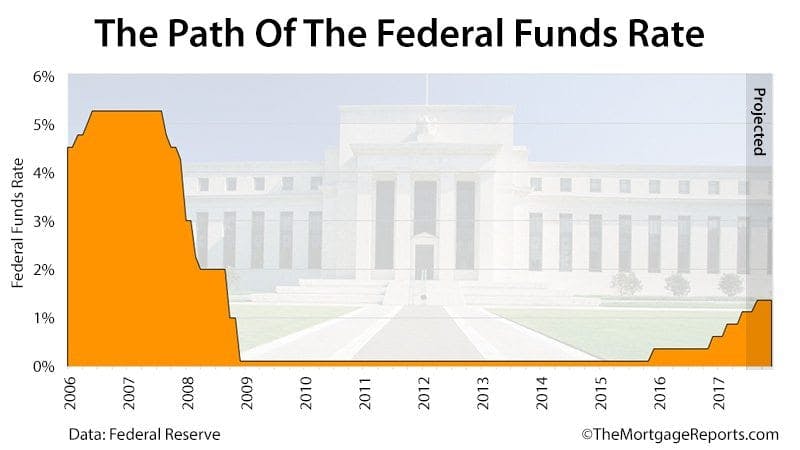

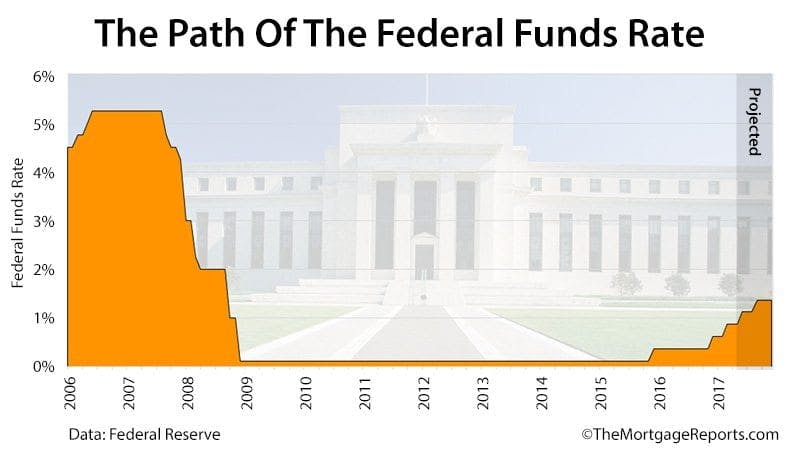

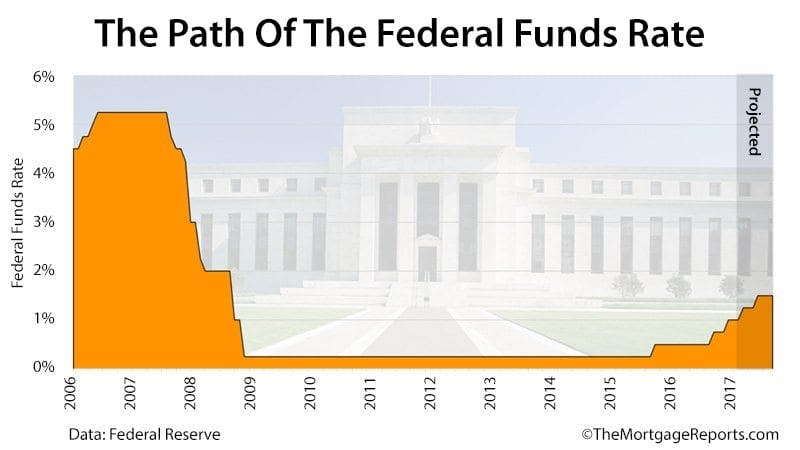

Federal ReserveSeptember 20, 2017Fed meeting: Committee says inflation not yet a concern, rates unchangedThis month's Fed meeting provided few surprises. No interest rate increase, but it's still on the table for December.

Federal ReserveJuly 26, 2017Fed Admits Inflation Is Low; Mortgage Rates FallThe Federal Reserve maintained its benchmark rate at its July meeting, but the group reiterated concern about low inflation, helping mortgage rates.

Federal ReserveJune 14, 2017Fed Hikes Rates, Says Economy Is On Solid GroundToday's Fed meeting resulted in a rate increase. This won't affect long-term mortgage rates, but will trickle up to increase rates on HELOCs, credit cards, and other loans tied to the Prime Rate.

Federal ReserveMay 3, 2017Federal Reserve Maintains Low Rates. No Hike Until At Least JuneThe Federal Reserve maintained its benchmark rate at its May meeting. No chance for another rate hike until at least June 2017. Analysis and forecast.

Federal ReserveMarch 15, 2017Federal Reserve Hikes Rates, But Mortgage Rates DropThe Federal Reserve raised the Fed Funds Rate to a range of 0.75-1.0% at its March meeting. Why, then, are mortgage rates dropping?