Conventional LoansFebruary 2, 20263% Down Payment Mortgages for First-Time Home BuyersLearn about 3% down payment mortgage options, including 3% down conventional loans and 3.5% down FHA loans.

Mortgage StrategyJanuary 5, 2026Self-Employed Mortgage Loan | Requirements 2026Self-employed and need a mortgage? Discover self-employed mortgage requirements, income documentation tips, and today’s top lender rates.

Mortgage ProductsJanuary 2, 2026Fannie Mae HomeReady Income Limits | 2026The Fannie Mae HomeReady loan helps low-income buyers with 3% down. Discover if you meet the HomeReady income limits and guidelines.

Real Estate NewsNovember 15, 2023Fannie Mae Extends Positive Rent Payment Pilot ProgramExplore how Fannie Mae's Positive Rent Payment program extension is empowering tenants and fostering financial well-being through positive credit reporting.

Mortgage ProductsSeptember 19, 2023Fannie Mae: Mortgage Programs and How They WorkEver wondered about Fannie Mae and its spectrum of "conforming" mortgages? Read on to discover your home loan options and eligibility criteria.

RefinanceJuly 19, 2021Refinance rates fall as Adverse Market Refi Fee is removedThe Adverse Market Refinance Fee made it more expensive to refinance over the last year. Now, that fee has been removed. Learn more here.

Mortgage NewsMarch 16, 2021New rule means higher fees for investment property mortgages and second homesA new rule from FHFA caused a sharp increase in investment property mortgage and second home mortgage fees. Here's what you need to know.

Mortgage RatesApril 15, 2019Mortgage rates: Almost everything you want to knowKnow more about mortgage rates, and you'll get a better rate. Understand how rates are made and how to best shop for FHA, VA, USDA, & conventional loans.

Mortgage ProductsDecember 11, 2018Fannie Mae’s mandatory waiting period after bankruptcy, short sale, & pre-foreclosure is just 2 yearsThe waiting period before you can make a mortgage application after a "significant derogatory event" has been cut by half. Get more on Fannie Mae's update.

Mortgage StrategyOctober 3, 2018This credit card rule makes mortgage qualification easierA change in the way credit card debt is calculated makes it easier for to get mortgage-qualified. Read more about the change and see today's live mortgage rates.

Mortgage ProductsJuly 14, 2017The 5-10 Properties program is for investors with more than 4 properties financedInvestor with more than 4 properties financed? Use Fannie Mae's standard 5-10 Properties Program. How to apply plus today's mortgage rates.

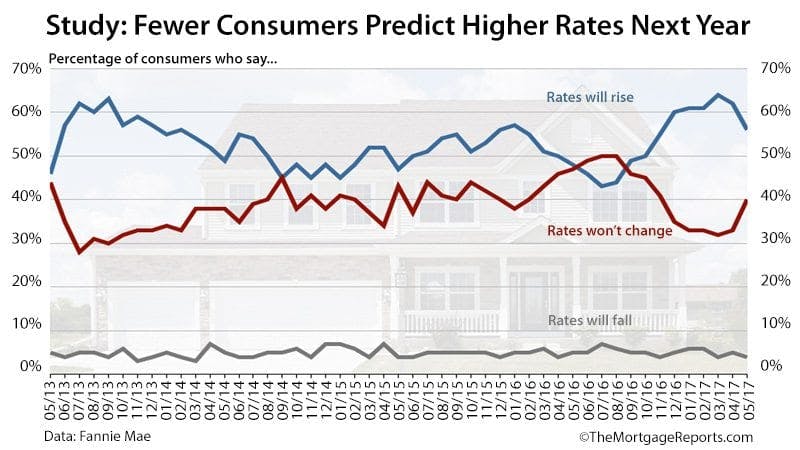

Mortgage NewsJune 13, 2017Consumers: Maybe Mortgage Rates Won’t Rise After AllA recent Fannie Mae survey shows a shift in consumer attitudes about mortgage rates. Twelve months from now, say survey takers, rates could be lower.

Mortgage ProductsJune 12, 2017Fannie Mae Just Increased What You Can BorrowFannie Mae just loosened up its guidelines, allowing some applicants to borrow with a 50 percent debt-to-income ratio.

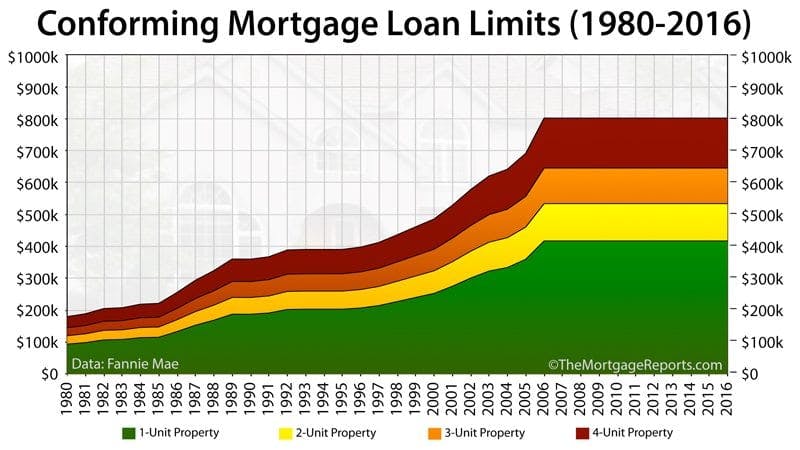

Conforming MortgagesMarch 14, 20172026 Mortgages Are Different: Fannie Mae Changes You Need To KnowConforming mortgages this year will be a little different, thanks to changes at Freddie Mac and Fannie Mae. Here are the ones most likely to affect you

Mortgage ProductsJuly 2, 2016The HomeStyle® Renovation Loan: A Less-Expensive Construction Loan Than The FHA 203k?Using the Fannie Mae HomeStyle® Renovation loan to finance home improvements can be cheaper and more efficient than the FHA 203k rehab loan. Read more.

Conventional LoansJune 6, 20164 conventional loans with low down paymentsWhen you want to make a low down payment, conventional mortgages can be less expensive and easier to access than FHA, VA, or USDA loans.

About MortgagesMay 31, 2016Private Mortgage Insurance (PMI) Is Neither “Good” Nor “Bad”Not sure whether you want to put 20% down on a home? It's okay if you don't. Frank talk about private mortgage insurance (PMI) and how it can help you buy.

Mortgage StrategyMarch 29, 2016Qualifying For A Mortgage Using Tip Income & GratuityNew, relaxed mortgage guidelines make it simpler for tip-earning workers across a host of industries to get mortgage home loan-qualified.

Mortgage ProductsJanuary 23, 2016Fannie Mae HomePath mortgage: low down payment, no appraisal needed, and no PMIAbout the Fannie Mae HomePath Mortgage program plus details for getting approved. Read more about HomePath. Get today's live mortgage rates.

Conforming MortgagesJanuary 19, 2016“Expensive” Homes Easier To Mortgage Under New Mortgage RulesFannie and Freddie have made it easier for home buyers in "high-cost" areas to get mortgage-approved. Rates are now lower and mortgage standards more loose.