Conforming MortgagesMay 9, 2022Conforming loan guide 2026: Requirements and loan limitsConforming loans are the most common type of mortgage. But what are they and how do they work? Use this conforming loan guide to learn more.

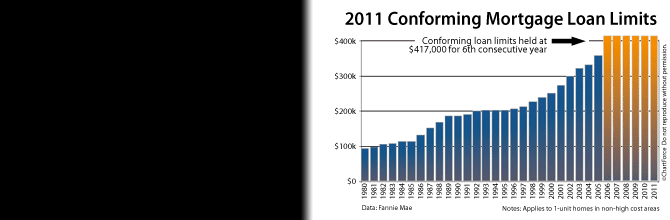

Conforming MortgagesNovember 30, 20102011 Conforming Mortgage Loan Limits By County, Including “Normal” and “High-Cost” AreasIn 2011 -- for the 6th consecutive year -- the single-family conforming mortgage loan limit will be $417,000. The "high-cost" area program is extended, too.