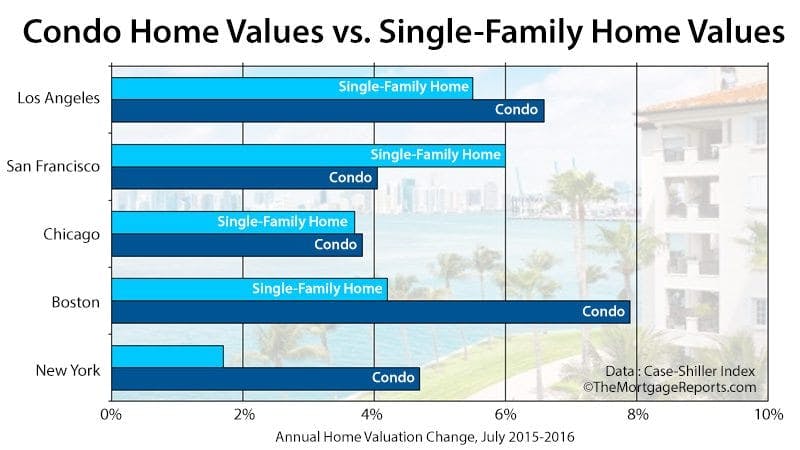

Real Estate NewsSeptember 28, 2016Condo Values Rising Fast In 5 Major MetrosIs a better to buy a condo or a single-family, detached home? Recently, condos have held value better. Analysis of the condo market, plus live condo mortgage rates.