It appears that lower mortgage rates come with a price. Closing costs rising in most states.

Can Your Closing Costs Be Lower?

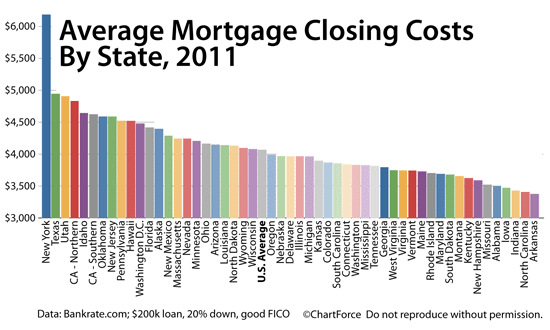

According to Bankrate.com’s 2011 Closing Cost Survey, average closing costs are higher by 9 percent this year, fueled by an increase in origination charges and third-party costs.

Origination charges include processing and underwriting, among other costs. Third-party costs include title search, title insurance and surveys fees.

Depending on where you live, though, your closing costs can vary.

For example, New York is the most expensive state in which to close a mortgage, averaging nearly $6,200 per transaction. Those are costs that can be paid as cash at closing; or added to the loan balance; or “built-in” to the mortgage rates.

Texas, the next-most-expensive state in which to close a mortgage averages $4,900 per loan.

Click here for a zero-cost mortgage rate quote

.

Drop Your Closing Costs To $0

Closing costs are expensive but don’t let that stop you from looking at a refinance. There’s a way to avoid paying them (sort of). You just have to ask the right questions.

See, traditionally, there’s two ways to cover your closing cost payments.

One, you could pay them with cash from your bank account at closing. You’d be paying with post-tax dollars and the monies would be gone from your account forever. And, even in states with low closing costs, like Maryland, that’s a lot of money.

Two, you could pay for costs using home equity. These are pre-tax dollars, but in a market in which equity’s at a premium, this, too, can be long-term costly. When you sell your home, you’ll get less back from the bank.

And that brings us to the third option — which is often the best option, too.

The zero-closing cost mortgage.

Zero-Closing Cost Mortgages

Zero-closing cost mortgages are exactly what they sound like — mortgages with no closing costs to the homeowner whatsoever. Loan balances don’t increase and loan costs aren’t “hidden” and/or added to your loan size.

The loans are truly “zero cost”.

Click here for a zero-cost mortgage rate quote

.

But nothing in life in free, however. In exchange for having your closing costs waived, your lender will ask you to take a slightly higher rate than the “market rate”. Depending on in which state you live and your loan size, this rate increase may be as much as 1/2 percent or as little as 1/8 percent.

In most cases, zero-cost mortgage rates are 0.250 basis points higher than the prevailing market rate. This makes the monthly payment higher, but not by much.

Example: At today’s rates, for every $300,000 borrowed on a 30-year fixed rate loan, a zero-cost mortgage rate costs $30 more per month than a full-cost loan.

If you lived in Washington D.C., in other words, where closing costs average $4,500, you would gladly spend $30 more per month to save $4,500 at your closing.

Want A Zero-Cost Mortgage Quote?

Today’s mortgage market is wild and unpredictable. We’ve seen big swings in rates on a day-to-day basis and there’s no promise rates won’t be lower 12-18 months from now.

The best way to hedge your risk against “refinancing too soon” is to refinance with no costs. You won’t get the absolute lowest rate, but you won’t be wasting money on closing fees, either.

It’s a perfect hedge for an imperfect market.

Time to make a move? Let us find the right mortgage for you

.