Refinance Your ARM To Another ARM: It’s A Valid Strategy

If you have an ARM loan, you probably chose it to save money, and you probably did save money. Typically, interest rates for the popular 5/1 ARM run about one percent lower than those of 30-year fixed-rate mortgages.

But if your introductory period is ending, you may be concerned about future rate increases. You could head them off if you refinance your ARM to another ARM.

Verify your new rateWhy Choose An ARM — Again?

You may be freaking out about the end of your introductory period with its low, fixed rate. And you might be sorely tempted to “set and forget” your loan with a new, fixed-rate mortgage.

You can certainly choose this product, but understand that you’ll pay a price. And the reasons for choosing a new ARM over an fixed loan may be as valid now as they were when you got your current home loan.

Open Your Eyes

Before you refinance your ARM, you need to know a couple of things:

- How long do you expect to keep your loan now?

- What are your ARM interest rate and payment likely to be?

- Will you save money by refinancing?

- Can you sleep at night without a fixed loan?

If the answer to the last question is a resounding “no,” get yourself to a lender and get yourself a fixed-rate refinance.

End of story.

However, if you’re a good sleeper and expect to have your home and your mortgage for just a few years more, you may save a ton, again, with a new 3/1, 5/1, 7/1 or 10/1 ARM.

Verify your new rateYour ARM’s Index, Margin And Caps

Your first step is determining what would happen to your ARM if it were adjusting today, and what it’s likely to do in the near future.

To do this, you need to look at your loan paperwork and find your loan’s index, margin and caps.

Suppose you have Fannie Mae’s popular 5/1 LIBOR ARM with two percent caps, a 1.5 percent margin and a five percent lifetime cap. Today’s LIBOR index is 1.80 percent, so if your loan were resetting today, your new rate would be 3.3 percent. If your current rate is 3.0 percent, your increase is only .3 percent, and that new rate is good for another year.

But what about subsequent years? Here are a few more figures for you.

- The median value of the 1-Year LIBOR over the last 20 years is 1.90 percent. If your loan were resetting based on that value, your new rate would be 3.4 percent.

- The highest rate your loan could hit at its next adjustment is 5.0 percent, because your adjustment cap is two percent.

- The highest rate your loan could reach in its lifetime is 8.0 percent, because its lifetime cap is five percent.

- The Federal Reserve believes that by the end of 2017, the average 30-year fixed-rate mortgage will rise to 4.6 percent, and 15-year fixed mortgage rates will hit 3.8 percent.

Right now, ARMs just don’t look that scary.

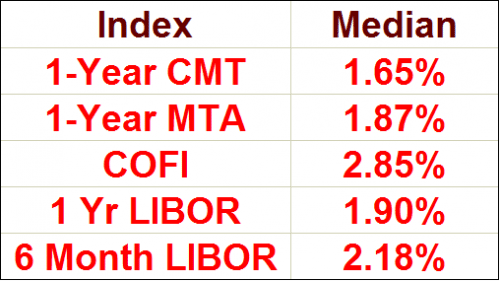

Popular ARM Indexes

Over the last 20 years, ARMs have performed pretty well for their borrowers. Here are the median values for some of the most widely-used ARM indexes.

ARM Vs Fixed Breakeven

Maybe after looking at ARM indexes and your own loan documents, you feel less worried about an impending reset. But if you want to extend your comfort zone a little, you can always refinance your ARM to a new one while rates are still low.

What Are Today’s Mortgage Rates?

Current mortgage rates still represent very good value, and continue to make homeownership highgly-affordable in the US. Ask your mortgage lender to show you today’s rates for fixed mortgages as well as ARMs fixed for three, five, seven or ten years.

Time to make a move? Let us find the right mortgage for you